The Other B Word

Budgeting is rather like eating healthily or exercising. Some people like to do it, but for others it’s a chore. And for many it’s a source of guilt. They think they should do it, but they don’t.

This article could be yet another telling the laggards how they will be much better people if they keep track of all their spending. But that’s hardly likely to make any more difference than other such articles.

As poet Robert Frost wrote: “Nobody was ever meant, to remember or invent, what he did with every cent.”

Instead, therefore, some tips for the less than enthusiastic budgeter:

1. Do you need to budget anyway?

If your income covers your expenses — including a satisfactory rate of saving if you want to save — then arguably you are budgeting anyway, in an informal way.

Don’t forget, though, to plan for expensive purchases such as a new car or a holiday. If you usually fund those out of savings, rather than borrowed money, over a lifetime you will save thousands of dollars in interest. (See sidebar: “2 ways to buy cars”)

However, if you cannot save as much as you would like to, or if you have debt of any kind, you’ll do yourself a big favour by budgeting at some level.

2. How much record-keeping is necessary?

If you’re disciplined, you may want to firstly estimate how much you spend in various categories, perhaps using our “Your Budget” list.)

Then either write down in a notebook how much you actually spend in each category over a few months, or compile a list using bank statements, cheque butts and credit card bills.

The numbers don’t need to be precise. If you don’t have good data, guess, and round off numbers to the nearest $100.

Compare your actual spending with your estimates. Wherever the actual is higher might be a good place to reduce your spending.

Too onerous? Try for a second-best plan. Succeeding at that is better than failing at a best plan.

Under this option, simply ask yourself as you spend money over a few weeks, “Did I really need or want that — or as much as that?”

If you can identify some unnecessary spending and cut back on it, that might be all it takes to greatly improve your financial well-being.

Two points that might make this easier:

- Experts say that if you want to change a habit, do something different daily for just a month. So set a goal for 30 days, rather than forever.

- If you cut back on spending that also harms your health, such as smoking, drinking too much or eating too much unhealthy food, you are killing two birds with one stone. You’re entitled to feel very virtuous about your saving!

3. Can every New Zealander cut their spending?

There’s no doubt that some people struggle to get by on their income. But a decade or two ago, we all got by happily without many items widely regarded as necessities these days.

It’s all a matter of expectations, which can be altered.

If you are spending just to keep up with your friends, stop to consider whether your friends really care if you have the latest whatever. If they do, how good is the friendship?

Budget advisers report that some people on extremely low incomes manage to save a little.

4. How can you save easily?

The most painless way for most people is to automatically transfer savings out of your bank account, on the day you are paid, into a savings account or other savings vehicle.

Start with a small amount. Then, whenever your income rises or expenses decrease, add perhaps half of the extra money to your regular savings.

If you get unexpected money, such as back pay, a bonus or even redundancy pay or an inheritance, by all means spend half of it but save the rest.

5. What are the secrets of goal setting?

- Make your goals specific, such as: Paying off your credit card debt in six months or a year; saving $10,000 for travel or a house deposit; or repaying your mortgage five or ten years early.

- Break down big goals into smaller chunks.

- Involve others. Discuss your goals with a partner or friend to make sure they are realistic. Talking to others also makes you more inclined to stick to your goals.

- Write your goals down, and mark your diary or calendar to check your progress regularly.

6. What if you fall by the wayside?

Don’t be too hard on yourself. Include a few treats in your budget.

If you miss a goal one month, don’t try to make up for it next month, unless that’s easy. If you often miss a goal, perhaps you should modify it, and build up later.

And be flexible. Circumstances change. You’ll know if you are being realistic about changing a goal or if you are just finding excuses. If it’s the latter, think about whom you are cheating.

7. What about emergency money?

It’s good to have some money slightly out of reach, that you can call on in emergencies. Otherwise, you can end up paying high interest on a loan.

Some ideas of where to keep the emergency money:

- In a savings account.

- In a 60-day term deposit. You can put the emergency spending on a credit card and repay it when the term deposit matures.

- In a revolving credit mortgage account.

- In a conventional mortgage. Pay extra off the mortgage, and arrange with the lender to borrow that money back whenever you need it.

An advantage of either of the last two: It’s equivalent to your emergency money earning the mortgage interest rate tax-free — an excellent return on savings, with low risk.

RULE NUMBER ONE

Try to never borrow to buy goods or services that won’t grow in value.

Regular borrowers are obviously living beyond their budgets. If you already have long-term credit card, hire purchase or other high-interest debt, your top financial priority should be repaying it. Otherwise you end up spending much more for the items you buy.

Remember: repaying debt improves your financial situation as much as an investment with an after-tax return the same as the debt interest rate.

For example, if your credit card charges 20 per cent interest, repaying credit card debt is like making a 20 per cent after-tax return on an investment. Fantastic!

YOUR BUDGET

INCOME

Wages or salary

Investment income

Income from rent or boarders

Other

SPENDING

Savings

Food and groceries

Alcohol, cigarettes etc.

Rent or mortgage payment

Rates

Home maintenance

Electricity, gas

Telephone

Insurance: Life, house and contents, health, car

Entertainment

Recreational activities

Magazines, newspapers etc

Computer costs

Subscriptions/membership fees

Clothes

Doctor visits and other medical costs

School fees

Children’s pocket money

Gifts, donations

Lawyer, accountant fees etc.

Holiday expenses

Car: payments or saving for next car

Petrol

Registration

Car maintenance

Public transport

Hire purchase payments

Credit card repayments

Other

Total Income:

Minus Total Spending:

Answer:

If the answer is negative, you need to find ways to boost your income or cut your spending.

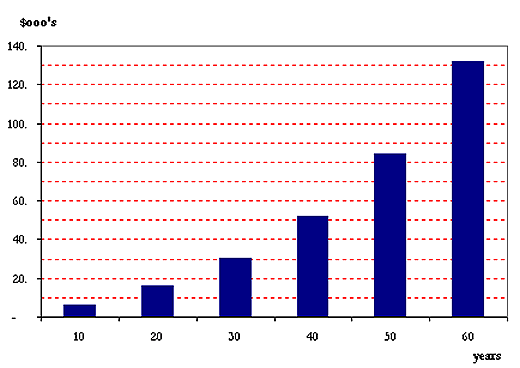

GRAPH: HOW SAVINGS OF $44 A MONTH WILL GROW

COMMENT ON GRAPH — TWO WAYS TO BUY CARS: THE POWER OF SAVING VS BORROWING

Let’s say you want to get a newer car every five years. And each time, you want to spend $5,000 more than the trade-in on your old car.

You either:

(a) Save for 5 years, earning 4 per cent a year after tax, and then upgrade the car. Savings each month: $76

(b) Don’t save, and borrow $5,000 when you buy each car at 15 per cent, which you pay off over the following five years. Payments each month: $120

Difference: $44 a month

If you choose (a), and each month you save the $44 at 4 per cent a year after tax, our graph shows how much extra money you will accumulate.

Notes:

- There is no allowance for inflation.

- If you want to spend $10,000 more on a new car each five years, multiply all numbers by 2.

- If you want to spend $20,000 more on a new car each five years, multiply all numbers by 4.

No paywalls or ads — just generous people like you. All Kiwis deserve accurate, unbiased financial guidance. So let’s keep it free. Can you help? Every bit makes a difference.

Mary Holm is a freelance journalist, a director of Financial Services Complaints Ltd (FSCL), a seminar presenter and a bestselling author on personal finance. From 2011 to 2019 she was a founding director of the Financial Markets Authority. Her opinions are personal, and do not reflect the position of any organisation in which she holds office. Mary’s advice is of a general nature, and she is not responsible for any loss that any reader may suffer from following it. Send questions to [email protected] or click here. Letters should not exceed 200 words. We won’t publish your name. Please provide a (preferably daytime) phone number. Unfortunately, Mary cannot answer all questions, correspond directly with readers, or give financial advice.