Highlights from Holm Truths

Over the next few weeks, this column will run highlights from Mary Holm’s quarterly newsletter Holm Truths. Mary’s regular Q&A column will resume on October 27.

STUFF AND HAPPINESS

A woman I know wasn’t sure what to do. Should she renovate her current house, or move to a cheaper suburb and buy a house that was already up to the minute? She preferred to stay put, but would have to borrow to renovate and wasn’t sure if she could afford to repay that debt.

“How about saving for a while until you can do up your house without borrowing?” I suggested.

“Oh no,” she replied. “The place has to be renovated now.” She ended up taking out the loan and struggling with the repayments — to say nothing of spending a considerable sum on interest.

In a recent survey by the Retirement Commission, more than a quarter of the respondents said their greatest difficulty around managing money was that they didn’t have enough. But how much is enough?

Did that woman really have to have the latest in interior design? Do others have to have a plasma TV, a new car every few years, or new clothes each season? Are many New Zealanders quite simply expecting a higher standard of living than they can afford?

And — the most important question of all — do all these things really make them happier in the long term?

I’m not denying that some families find it hard to buy their children a second pair of shoes. These days in New Zealand, it’s reasonable to expect kids to have alternative footwear.

Above that income level, though, there are many people who say they can’t save for retirement — or can’t save much for retirement — because they “need” to buy things they don’t need.

That’s their choice. But I think it’s worthwhile to challenge that thinking. Those who are willing to change their ways a little may find themselves facing a much more fun-filled and comfortable retirement.

In a telling study, students at Harvard University were asked whether they would prefer:

(a) $50,000 a year while others got half that, or

(b) $100,000 a year while others got twice as much.

More than half chose (a).

“Other studies confirm that people are often more concerned about their income relative to others’ than about their absolute income,” said the Economist magazine. “Pleasure at your own pay rise can vanish when you learn that a colleague has been given a much bigger one.”

It’s too easy to dismiss this tendency as a pathetic preoccupation with keeping up with the Joneses, or rather keeping ahead of the Joneses. Life is, indeed, simpler if you have about as much money as the people you socialize with — whatever that level is.

Ask anyone who has changed countries and in the process switched to a lower standard of living. Often they will say they had just as good a time in the new country, if not better, as long as they mixed with people on similar incomes. They could all afford the same big night out.

But we can take this thinking too far. Would your friends drop you if your coat, car or carpet weren’t as flash as theirs? If you think they might, do you want them as friends anyway?

What about your own feelings — the excitement of the first night you watch TV on your new big screen, or the first time you drive your new car with all its features? Research shows us what we already know. We are happier at first, but we adjust quickly to such changes, and shortly afterwards we are no happier than we were before.

Let’s look at what we find in a typical middle class house that we wouldn’t have found a generation or so ago: a family room, more than one bathroom, a walk-in double garage, at least one computer, a fancy stereo, dishwasher, microwave, second TV set, many phones, and so on.

Despite the fact that families are smaller, homes are usually much bigger. The average 1977 house was 127 square metres, compared with 175 today, according to the Department of Statistics.

Also, we are much more likely to have more than one car per family, our bach is probably much more luxurious, and overseas travel has soared.

Admittedly, some of these items are cheaper than they were for our parents, after we adjust for inflation. But the price of the most expensive item of all, the home, has risen more than inflation, and so have some other items.

Are we happier with all this extra stuff? That’s hard to measure, but it’s certainly not clear that we are.

Before you buy another “must have” item that you don’t really need — and particularly before you borrow to buy it and thus end up paying more for it — stop and think.

If you halve your spending on such items over the years, and put the saved money into retirement savings, you’ll be freer with your spending at a stage in life when you’ll have more time to enjoy what you buy.

What’s more, your friends might appreciate your lowering the standards for them, too!

HE WHO HESITATES IS RICHER

Six questions to ask yourself before making a major purchase:

- Do I really need this?

- If not, will I regard it as a worthwhile purchase in several months’ time, or would it be better to save the money for a future purchase or even retirement?

- Do I have the money to buy it without having to borrow?

- If not, is it feasible to save until I’ve got the money — letting interest work for me instead of against me.

- If I must have the item now, how can I borrow at the lowest possible interest rate?

- What will I give up in order to repay the loan as fast as possible?

UNASSUMING BILLIONAIRES

Some of the world’s richest people certainly live it up. But others live it down.

Examples:

- Incredibly successful share investor Warren Buffett is the world’s second richest man, according to Forbes. But he still lives in the house in suburban Omaha, Nebraska, that he bought in 1957. (By the way, Forbes names Microsoft’s Bill Gates as richest, although other publications put Mexican Carlos Slim Helu ahead of both Gates and Buffett).

- The founder of IKEA furniture stores, Swede Ingvar Kamprad, comes fourth on Forbes’ list. He drives a 15-year-old car and flies economy class, according to The Scotsman.

- Ken Thomson, whose media conglomerate made him easily Canada’s richest man and the world’s ninth richest before his recent death, was sometimes spotted in line at his local supermarket. He is said to have used store coupons and bought bread in bulk when it went on sale.

- Li Ka-Shing, whose company a year or so ago discussed a possible joint venture with Christchurch City Council to run the port of Lyttelton, is Forbes’ ninth richest man. He prefers cheap shoes and plastic watches, according to Herald reports.

Others lower down the rich list are similar. In their thought-provoking book “The Millionaire Next Door”, Thomas Stanley and William Danko point out that many millionaires got rich by not spending much. Indeed, some of them, like Buffett, still live in “the house next door” and few people know of their wealth.

As author and scriptwriter Jonathan Clements puts it: “The folks with the big house, fancy cars and designer clothes are, no doubt, loaded. But they may be loaded with debt.”

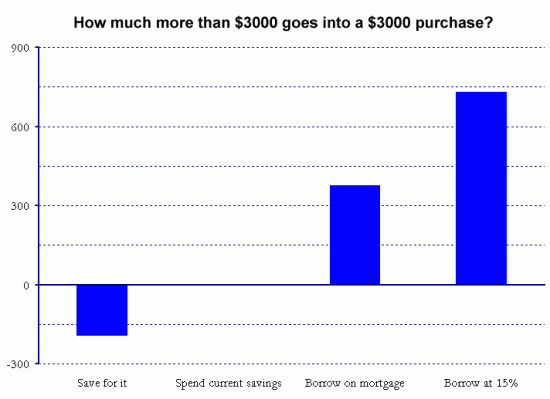

Let’s say you really want to buy a $3,000 television set. If you have enough money to buy it out of your savings, that’s great. If not, you have several options:

- Save up for it. In our graph, we assume you save $78 a month, earning interest at 4.5 per cent a year after tax, for three years. That would earn you about $190 in interest. So you would have to put in about $2,810 of your own money to get a total of $3,000. Your extra “spending” is minus $190!

- Add $3,000 to your mortgage and buy the TV. Then pay off that $3,000 over three years, while paying 8 per cent interest on it. Your monthly payments would be $94, and you would pay a total of $3,384 over the period — extra spending of $384.

- Take out a $3,000 personal loan at 15 per cent to buy the TV. Again, we assume the loan is repaid in three years. Your monthly payments would be $104, and you would pay a total of $3,744 over the period — extra spending of $744.

With the second two options, of course, you have the pleasure of watching the TV sooner. But you pay quite a high price for that pleasure. The difference between the cheapest and dearest options is $934 — almost a third again of the $3,000!

Note that if you fund a purchase by adding to your mortgage, it’s a good idea to pay off that extra money as fast as possible. If you simply pay it off along with the rest of the mortgage over many more years, you will pay much more interest on it.

No paywalls or ads — just generous people like you. All Kiwis deserve accurate, unbiased financial guidance. So let’s keep it free. Can you help? Every bit makes a difference.

Mary Holm is a freelance journalist, a director of Financial Services Complaints Ltd (FSCL), a seminar presenter and a bestselling author on personal finance. From 2011 to 2019 she was a founding director of the Financial Markets Authority. Her opinions are personal, and do not reflect the position of any organisation in which she holds office. Mary’s advice is of a general nature, and she is not responsible for any loss that any reader may suffer from following it. Send questions to [email protected] or click here. Letters should not exceed 200 words. We won’t publish your name. Please provide a (preferably daytime) phone number. Unfortunately, Mary cannot answer all questions, correspond directly with readers, or give financial advice.